The AI efficiency wave promises to reshape how freight brokers and forwarders operate – but the gains won’t flow automatically to incumbents. The answer lies in who owns the intelligence layer.

A $35M company is about to become a $22.5M company

The numbers are clarifying. Take a freight broker or forwarder doing $100M in revenue: 15% gross margins, 5% EBITDA, valued at a typical 7x multiple – call it $35M of enterprise value. Labor runs around 60% of gross profit, or $9M. Now introduce an AI platform that eliminates half that headcount. On the surface, a win: $4.5M in expense gone.

But here is where the math turns uncomfortable. If the forwarder doesn’t own the models or the technology, it is no longer an operating company in any meaningful sense. It has become a sales agent – a relationship layer resting on someone else’s infrastructure. The multiple compresses from 7x to somewhere between 4x and 5x EBITDA. That $35M enterprise value slips to roughly $22.5M.

BEFORE AI

$35M

7× EBITDA multiple

AFTER FULL OUTSOURCE

$22.5M

4–5× compressed multiple

AI VENDOR CAPTURE

$36M

8× ARR on $4.5M payroll

Meanwhile, the AI vendor – who now holds the $4.5M that was once the forwarder’s payroll – attracts an 8x revenue multiple from venture investors. The same freight, the same customers, the same book of business: collectively worth $58.5M across two entities. Enterprise value created from thin air. But none of that upside returned to the forwarder who built the customer relationships in the first place.

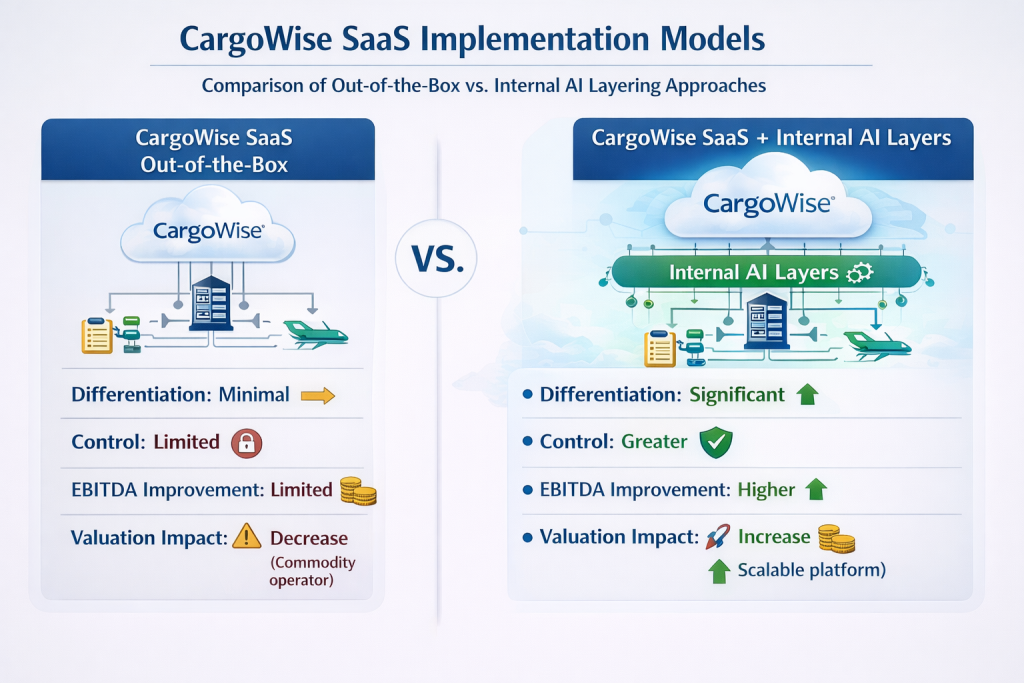

The dual-path approach: the only strategy that retains the value

The strategic error most operators will make is treating AI transformation as a binary choice – either adopt an external platform wholesale, or do nothing. The correct framing is a deliberately bifurcated architecture: one path for commodity tasks, an entirely separate path for proprietary ones.

PATH ONE · EXTERNAL HOSTING

Commodity & repetitive tasks

Document parsing, track-and-trace queries, rate lookups, status updates. These are high-volume, low-differentiation tasks. Outsourcing them to external AI platforms is rational – the data involved carries low strategic value and the cost savings are real.

PATH TWO · INTERNAL HOSTING

Proprietary workflows & intelligence

Routing logic, exception handling, margin decisions, carrier relationship scoring, customer-specific preferences. This is where years of transactional data produce genuinely defensible models. These tasks must be hosted internally – on infrastructure the forwarder owns and controls.

This distinction matters beyond simple expense accounting. Freight forwarders have always been protective of where their data lives – lanes, rates, shipper behavior, carrier relationships represent their operating advantage. The AI era extends that concern. It is no longer just a question of where the data is stored, but of where the process runs and who trains on it over time.

“The forwarder that trains proprietary models on years of its own transactional data owns something a generic AI vendor cannot replicate – or price-raise away.”

There is a second, longer-term risk that the dual-path approach addresses directly. Several AI platforms have signalled – through investor disclosures and pricing roadmaps – an intent to capture the full value of replaced labor as ARR over time. That means the $4.5M in cost savings a forwarder enjoys today may become $4.5M in higher software costs tomorrow. The only defence is to own a portion of the stack that cannot be priced against you.

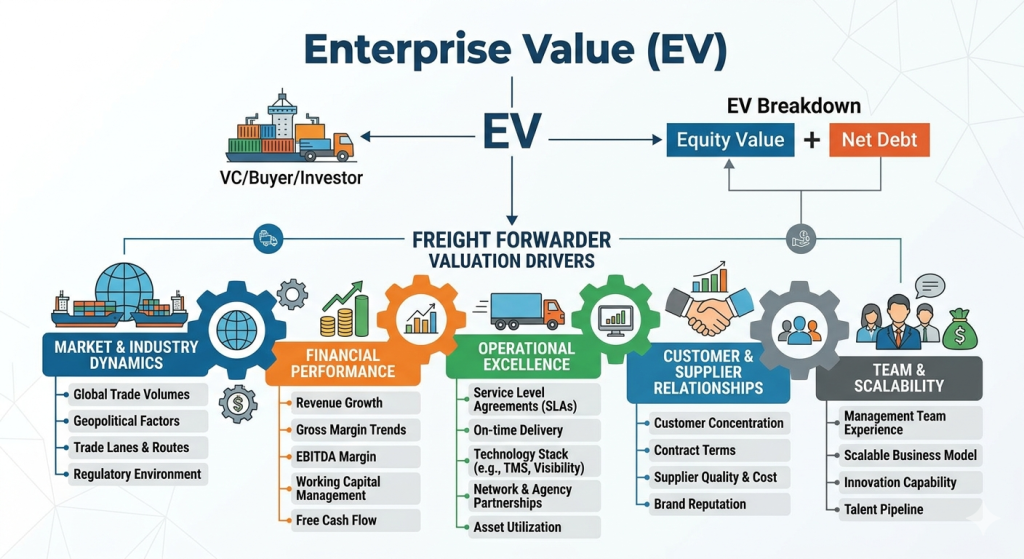

A forwarder that builds internal AI capability around its proprietary workflows is no longer purely an operating business. It holds a technology asset embedded inside a services company – and that combination is what commands a higher multiple. The question of whether non-asset services businesses can participate in the tech-style valuation uplift the article poses has a clean answer: yes, but only conditionally. The condition is ownership of the intelligence layer.

Key conclusions

Full AI outsourcing compresses freight forwarder valuations – savings flow upstream to vendors, not to operators.

The dual-path architecture – external hosting for commodity tasks, internal for proprietary workflows – is the only approach that retains strategic value.

Freight data is the model. Forwarders that train on their own transactional history own a moat that external platforms cannot replicate.

Data sovereignty must now extend beyond storage to process: who runs the logic matters as much as where the data lives.

Tech-style valuation multiples are available to services businesses – but only to those that own the intelligence layer, not those who rent it.

The operators best positioned to thread this needle are mid-to-large forwarders with the capital to invest in internal AI infrastructure. Smaller players face real multiple compression risk.