Introduction

Over the past decade, a new generation of “digital freight forwarders” promised to reinvent logistics. With modern interfaces, automated booking flows, real-time dashboards, and AI-driven rate comparisons, they positioned themselves as technology companies operating in freight.

The assumption was clear: digitize the process, remove inefficiencies, scale rapidly — and profitability would follow.

Yet several high-profile digital players have faced layoffs, valuation cuts, strategic pivots, or closures. The problem was not a lack of technology. The problem was forgetting the economics of freight.

The Illusion: If It’s Digital, It Must Be Better

Companies such as Flexport, Forto (formerly Freighthub), Xeneta, and Haven built models centered around:

- Automation

- Platform visibility

- Data-driven rate comparisons

- Reduced manual intervention

Technologically, these models were impressive. Operationally, they improved transparency and efficiency.

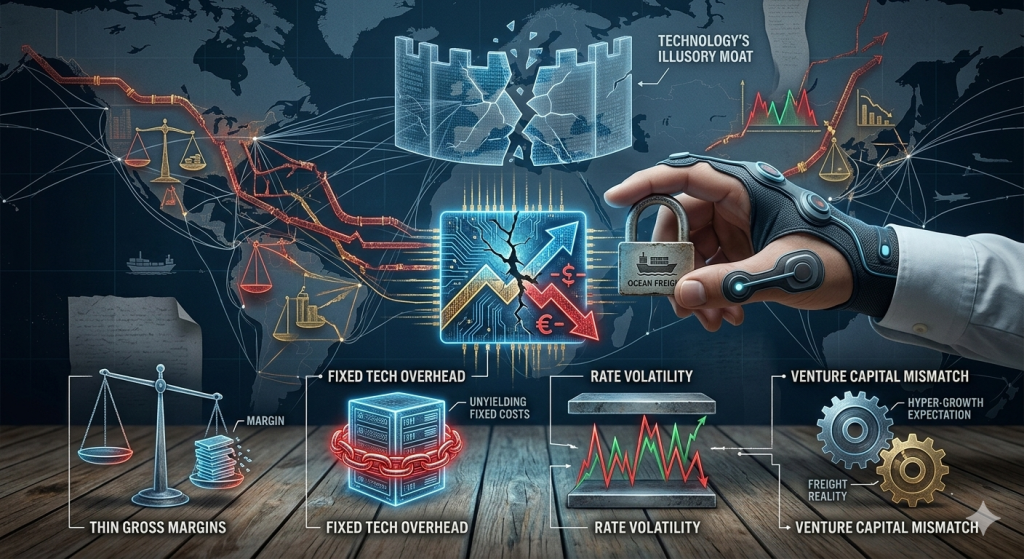

But freight forwarding is not a software business. It is a cyclical, capital-intensive, low-margin industry.

Digitization improves execution. It does not rewrite industry structure.

Freight Has Structural Realities

Freight forwarding operates under constraints that technology alone cannot eliminate:

- Thin gross margins

- High working capital requirements

- Exposure to volatile carrier rates

- Customer price sensitivity

- Credit risk

- Relationship-driven procurement

When ocean and air rates surged during the pandemic, digital forwarders scaled aggressively. Revenue rose rapidly. Valuations expanded.

When rates normalized, the underlying economics reappeared.

Gross profit per shipment fell. Volume growth slowed. Fixed tech overhead remained.

Technology did not protect them from rate cycles.

The Venture Capital Mismatch

Many digital forwarders were venture-backed.

Venture capital expects:

- Rapid market capture

- High growth multiples

- Network effects

- Strong operating leverage

Freight forwarding, however, delivers:

- 5–10% margins in good years

- Enterprise sales cycles

- Conservative switching behavior

- Volatile earnings

This mismatch creates tension. To meet growth targets, digital forwarders often prioritize volume expansion over margin discipline. In freight, volume without pricing power can destroy profitability.

Traditional forwarders, by contrast, often grow slower but guard margins more carefully.

Technology Adds Cost Before It Adds Advantage

Another misconception is that digital means lean.

In reality, digital forwarders carry:

- Large engineering teams

- Product and UX staff

- Data infrastructure expenses

- Marketing and brand spend

These are fixed costs.

When margins compress, high fixed costs become dangerous. Traditional forwarders can reduce operational staff quickly in downturns. Tech-heavy models have less flexibility.

Digitization reduces manual labor, but if the tech overhead is too high relative to freight margins, the cost structure becomes unstable.

Freight Is Not Purely Transactional

Freight is full of exceptions:

- Port congestion

- Sanctions and compliance issues

- Space allocation politics

- Disputes over demurrage and detention

- Credit and liability negotiations

Shippers still value escalation handling, commercial judgment, and relationships with carriers and authorities.

Digital interfaces may simplify booking, but when complexity arises — and it always does — the real value lies in operational depth and risk management.

If technology replaces too much of the relationship layer without strengthening the control layer, the model becomes fragile.

What Was Overestimated

Digital forwarders often assumed:

- Shippers would switch primarily for better UI

- Carriers would fully expose rates digitally

- Automation would dramatically increase margins

- Freight could scale like software

In practice:

- Switching costs in freight are operationally high

- Carrier relationships remain strategic

- Margin gains from automation are incremental, not transformative

- Freight cycles compress profitability regardless of platform quality

Technology is necessary infrastructure. It is not a structural moat.

The Core Problem: Ignoring Economics

The central issue is not digitization failure. It is economic misalignment.

Freight profitability depends on:

- Pricing discipline

- Procurement leverage

- Customer mix

- Working capital control

- Risk management

- Cost flexibility

If these fundamentals are weak, digitization simply accelerates volume through an unprofitable engine.

You can build the most elegant booking interface in the industry.

If you misprice risk or overextend working capital, the model breaks.

The Real Lesson

Digital freight forwarders are not failing because they are digital.

They struggle when they assume digitization replaces freight fundamentals.

The sustainable model likely lies in combining:

- Strong economic discipline

- Lean but effective digitization

- Careful cost control

- Operational depth

- Capital resilience

Technology should strengthen margins, not mask them.

Freight remains what it has always been:

A cyclical, risk-sensitive, relationship-heavy industry.

Digitization changes how it is executed.

It does not change what drives profit.

Leave a Reply

You must be logged in to post a comment.