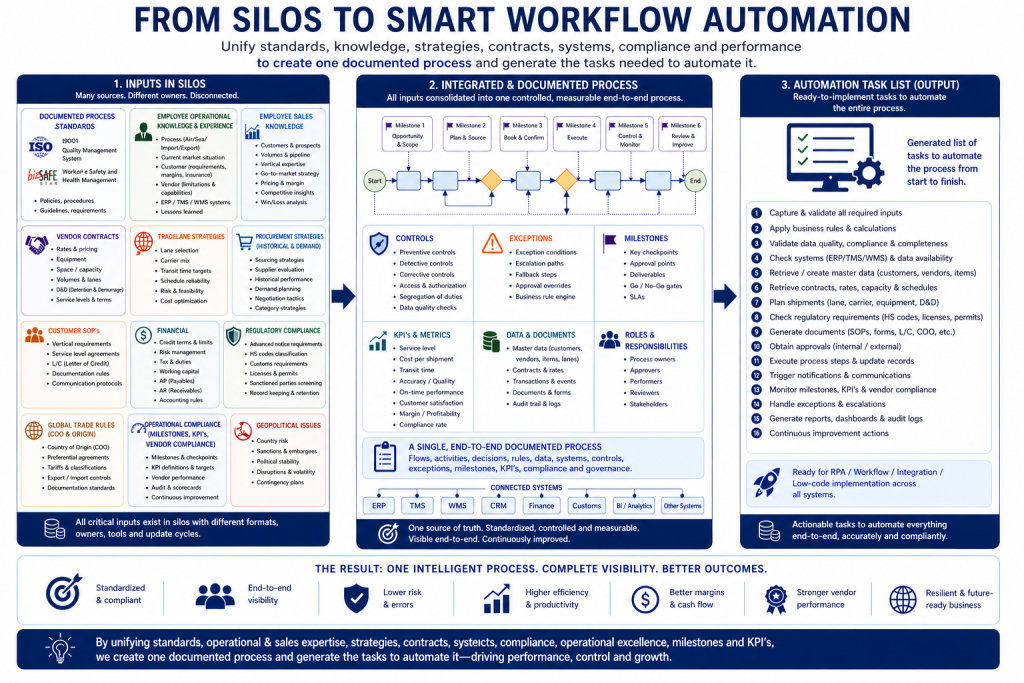

There’s a growing frustration around how slowly the freight forwarding and logistics industry is adopting automation. Many IT vendors have entered the space with strong expectations, only to step back after struggling to gain traction. From the outside, it often looks like resistance to change. From the inside, the reality is more complicated.

At first glance, freight forwarding appears highly repetitive. Emails, documents, shipment updates, billing. It feels like an ideal candidate for automation. But once you look closer, the process is not just a sequence of tasks. It’s a web of decisions, exceptions, and dependencies.

A single shipment can involve:

Customer-specific SOPs and service expectations

Vendor constraints on space, equipment, and routing

Rapidly changing market conditions

Financial considerations such as margins, credit limits, and working capital

Regulatory requirements including customs, licenses, and trade compliance

System limitations across ERP, TMS, and WMS platforms

Geopolitical disruptions affecting routes and costs

None of this sits in one place.

The real challenge is not technology. It’s fragmentation.

Knowledge is spread across:

Operations teams who understand how shipments actually move

Sales teams who know the customer, volumes, and pricing strategy

Procurement teams managing carriers and contracts

Finance teams controlling risk and revenue recognition

Compliance teams managing regulatory exposure

Each group holds a piece of the process. Very little of it is fully documented end-to-end.

This creates two core problems.

First, processes are often incomplete. What exists in SOPs typically covers the “standard case,” but not the real-world exceptions that happen daily. Automation struggles in environments where exceptions are not clearly defined.

Second, decision-making is embedded in people, not systems. Experienced operators constantly make judgment calls based on context. Vendor reliability, customer sensitivity, margin pressure, or shipment urgency. These decisions are rarely written down, but they are critical to execution.

When IT vendors try to automate such environments, they face a moving target. What looks like a simple workflow quickly expands into a complex set of rules, exceptions, and dependencies. Implementation timelines stretch. Scope increases. Confidence drops. Eventually, projects stall or are abandoned.

This is why many automation initiatives in freight forwarding fail before they even begin. Not because the technology doesn’t work, but because the process is not ready.

There is a way forward, but it requires a shift in approach.

Automation should not start with tools. It should start with clarity.

Companies need to:

Document processes beyond the standard flow, including exceptions and controls

Consolidate knowledge from operations, sales, procurement, finance, and compliance

Define decision logic where possible, and clearly separate what remains judgment-based

Align data structures across systems

Establish milestones, KPIs, and ownership

Only then does automation become practical.

When this foundation is in place, something changes. The process becomes visible. Dependencies are understood. Tasks can be broken down. At that point, automation is no longer an abstract concept. It becomes a series of clearly defined steps that can be implemented.

The industry is not slow because it resists automation. It’s slow because the underlying processes are complex, fragmented, and often undocumented.

Once that is addressed, automation doesn’t just become possible. It becomes inevitable.

The AI efficiency wave promises to reshape how freight brokers and forwarders operate – but the gains won’t flow automatically to incumbents. The answer lies in who owns the intelligence layer.

A $35M company is about to become a $22.5M company

The numbers are clarifying. Take a freight broker or forwarder doing $100M in revenue: 15% gross margins, 5% EBITDA, valued at a typical 7x multiple – call it $35M of enterprise value. Labor runs around 60% of gross profit, or $9M. Now introduce an AI platform that eliminates half that headcount. On the surface, a win: $4.5M in expense gone.

But here is where the math turns uncomfortable. If the forwarder doesn’t own the models or the technology, it is no longer an operating company in any meaningful sense. It has become a sales agent – a relationship layer resting on someone else’s infrastructure. The multiple compresses from 7x to somewhere between 4x and 5x EBITDA. That $35M enterprise value slips to roughly $22.5M.

BEFORE AI

$35M

7× EBITDA multiple

AFTER FULL OUTSOURCE

$22.5M

4–5× compressed multiple

AI VENDOR CAPTURE

$36M

8× ARR on $4.5M payroll

Meanwhile, the AI vendor – who now holds the $4.5M that was once the forwarder’s payroll – attracts an 8x revenue multiple from venture investors. The same freight, the same customers, the same book of business: collectively worth $58.5M across two entities. Enterprise value created from thin air. But none of that upside returned to the forwarder who built the customer relationships in the first place.

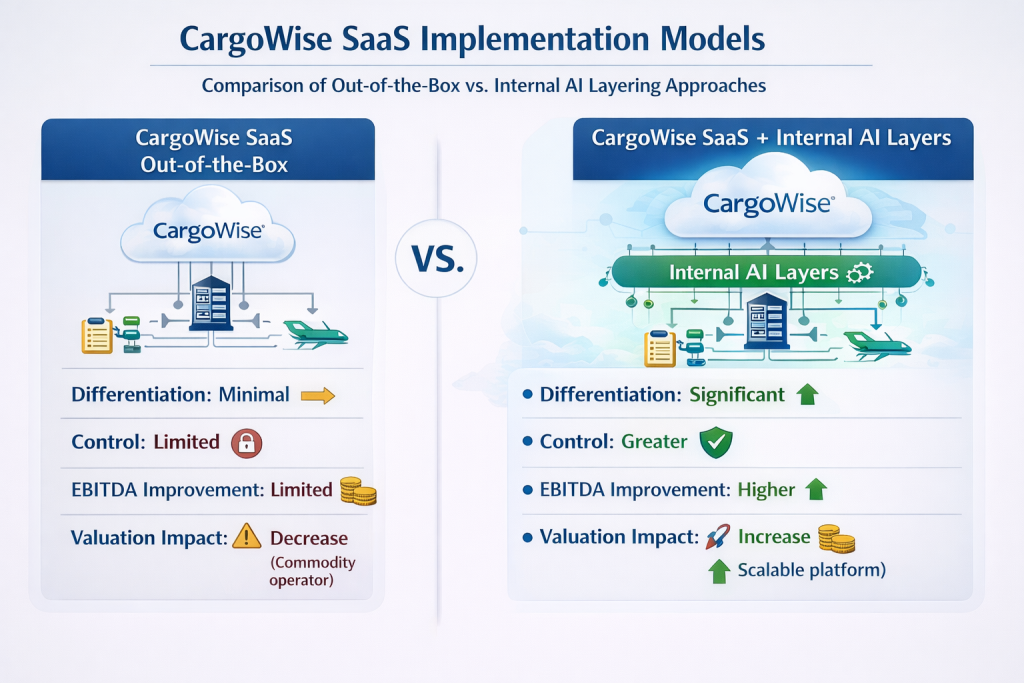

The dual-path approach: the only strategy that retains the value

The strategic error most operators will make is treating AI transformation as a binary choice – either adopt an external platform wholesale, or do nothing. The correct framing is a deliberately bifurcated architecture: one path for commodity tasks, an entirely separate path for proprietary ones.

PATH ONE · EXTERNAL HOSTING

Commodity & repetitive tasks

Document parsing, track-and-trace queries, rate lookups, status updates. These are high-volume, low-differentiation tasks. Outsourcing them to external AI platforms is rational – the data involved carries low strategic value and the cost savings are real.

PATH TWO · INTERNAL HOSTING

Proprietary workflows & intelligence

Routing logic, exception handling, margin decisions, carrier relationship scoring, customer-specific preferences. This is where years of transactional data produce genuinely defensible models. These tasks must be hosted internally – on infrastructure the forwarder owns and controls.

This distinction matters beyond simple expense accounting. Freight forwarders have always been protective of where their data lives – lanes, rates, shipper behavior, carrier relationships represent their operating advantage. The AI era extends that concern. It is no longer just a question of where the data is stored, but of where the process runs and who trains on it over time.

“The forwarder that trains proprietary models on years of its own transactional data owns something a generic AI vendor cannot replicate – or price-raise away.”

There is a second, longer-term risk that the dual-path approach addresses directly. Several AI platforms have signalled – through investor disclosures and pricing roadmaps – an intent to capture the full value of replaced labor as ARR over time. That means the $4.5M in cost savings a forwarder enjoys today may become $4.5M in higher software costs tomorrow. The only defence is to own a portion of the stack that cannot be priced against you.

A forwarder that builds internal AI capability around its proprietary workflows is no longer purely an operating business. It holds a technology asset embedded inside a services company – and that combination is what commands a higher multiple. The question of whether non-asset services businesses can participate in the tech-style valuation uplift the article poses has a clean answer: yes, but only conditionally. The condition is ownership of the intelligence layer.

Key conclusions

Full AI outsourcing compresses freight forwarder valuations – savings flow upstream to vendors, not to operators.

The dual-path architecture – external hosting for commodity tasks, internal for proprietary workflows – is the only approach that retains strategic value.

Freight data is the model. Forwarders that train on their own transactional history own a moat that external platforms cannot replicate.

Data sovereignty must now extend beyond storage to process: who runs the logic matters as much as where the data lives.

Tech-style valuation multiples are available to services businesses – but only to those that own the intelligence layer, not those who rent it.

The operators best positioned to thread this needle are mid-to-large forwarders with the capital to invest in internal AI infrastructure. Smaller players face real multiple compression risk.

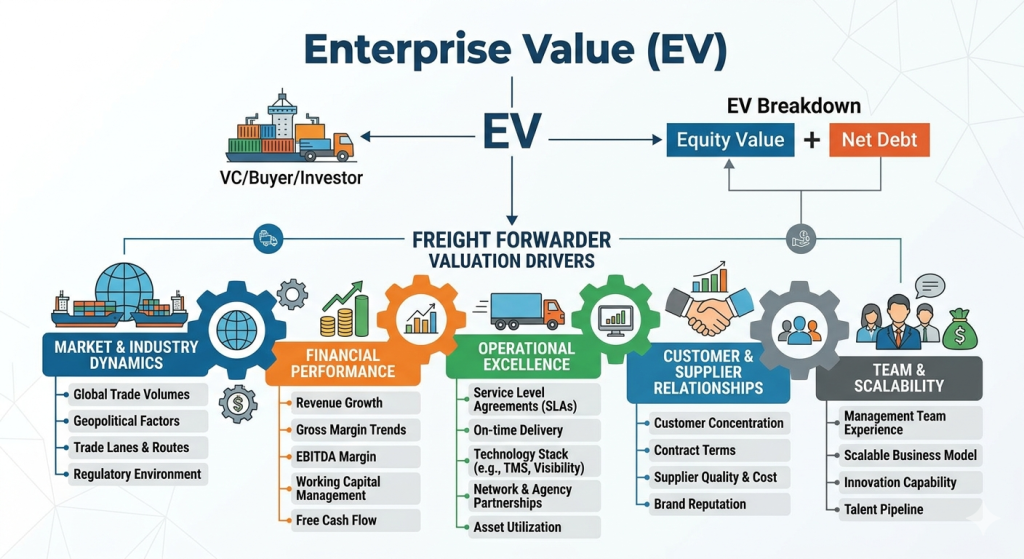

The freight forwarding industry has long been viewed through a transactional lens — margins are thin, volumes fluctuate with trade cycles, and differentiation is notoriously hard to articulate. Yet deal activity in the sector has intensified, with strategic buyers and private equity firms paying increasingly varied multiples for businesses that look, on the surface, remarkably similar. A forwarder turning $100 million in revenue at a 5% EBITDA margin might trade at 5x. Another with comparable financials might fetch 10x. The difference rarely comes down to the numbers themselves. It comes down to what sits behind them.

Enterprise value in freight forwarding is not simply a function of earnings. It is a function of the quality, defensibility, and scalability of those earnings. Investors and acquirers are asking a different set of questions than they did a decade ago — questions about data ownership, technology architecture, customer stickiness, and whether the business can grow without a proportional increase in headcount. Understanding how sophisticated buyers decompose value is no longer just useful for founders preparing for an exit. It is essential for any operator thinking seriously about how to build a business worth owning.

What Investors Are Actually Measuring

Financial performance: the starting point, not the conclusion

Every diligence process begins with the financials, but experienced buyers move through them quickly. Revenue growth rate, gross margin percentage, EBITDA conversion, and free cash flow generation are threshold questions, not differentiators. What matters more is the trajectory and the composition.

A forwarder growing at 15% annually on contracted revenue is a fundamentally different business from one growing at 20% on spot freight during a rate spike. Working capital management tells a similarly revealing story — a business with a tight cash conversion cycle signals operational discipline and pricing power, while a stretched debtor book often points to customer concentration problems or weak commercial terms. These dynamics are well understood by PE buyers, who will normalise EBITDA, stress-test margins across cycle scenarios, and build a clear picture of sustainable earnings before any multiple conversation begins.

Revenue quality: the first real differentiator

Once the financials are understood, attention shifts rapidly to revenue quality — and this is where many freight forwarders are surprised by how deeply buyers probe. Customer concentration is the most immediate concern. A top-ten customer representing more than 20% of gross profit introduces meaningful risk, particularly where that relationship is held personally by a founder or senior operator rather than embedded institutionally.

Beyond concentration, buyers examine the contract versus spot revenue mix, average customer tenure, churn rates, and evidence of wallet share expansion over time. A portfolio of long-tenured customers across diverse verticals and trade lanes, each deepening their commercial relationship with the forwarder year over year, is the kind of revenue quality that genuinely moves multiples. It suggests the business is providing something customers cannot easily replicate elsewhere — and that is the essence of defensibility.

Operational capability: scalability is the question

Operational strength in freight forwarding has historically been measured in execution reliability — on-time performance, exception resolution, carrier relationship depth. These remain important, but the investor lens has sharpened considerably. The question is no longer simply whether the business operates well. It is whether the business can scale its operations without scaling its cost base at the same rate.

Forwarders with highly standardised processes, documented SOPs, and systematic exception handling demonstrate the kind of operational architecture that supports margin expansion as volume grows. Those relying on tribal knowledge, individual expertise, and manual intervention at every inflection point face a structural ceiling. Buyers can see this ceiling clearly in the data — it shows up in headcount-to-revenue ratios, in SLA variance across customer accounts, and in the time and cost required to onboard new business. Process maturity is, in this sense, a form of leverage.

Technology and data: the emerging valuation frontier

No component of freight forwarder valuation has shifted more dramatically in the past five years than technology and data. What was once assessed as a hygiene factor — does the business have a functioning TMS? — has become a primary lens through which differentiation and defensibility are evaluated.

The critical distinction investors now draw is between forwarders that use technology and those that own it. A business running on vendor-provided platforms, with decision logic residing in external systems, has outsourced a meaningful portion of its operational intelligence. It may be efficient, but it is not differentiated — and its dependency on third-party tools creates both margin risk and switching cost vulnerability in the wrong direction. Conversely, a forwarder that has built proprietary workflows, owns its pricing and rating logic, has deep API connectivity with key customers, and generates data that compounds in value over time is building something qualitatively different. That compound data effect — where every shipment makes the next decision slightly better — is one of the few genuine moats available in this industry, and sophisticated buyers price it accordingly.

The rise of AI has added a further dimension to this assessment. Investors are now asking not just whether a forwarder has adopted AI, but where the AI capability resides. An AI tool licensed from a vendor improves efficiency but transfers value upstream. An AI capability built on proprietary data and embedded in internal workflows is a genuine asset. The distinction matters enormously to valuation.

People and management: the risk layer

However strong the financials and however impressive the technology architecture, people risk remains one of the most common reasons deal processes stall or multiples compress at the final stage. Key person dependency is endemic in freight forwarding, where customer relationships and carrier networks are frequently held by individuals rather than institutions. A business where the departure of one or two senior operators would materially affect revenue is a business with a structural fragility that no amount of EBITDA normalisation can fully address.

Buyers look for management bench strength, evidence of deliberate succession planning, incentive structures that align the leadership team with long-term outcomes, and a culture of accountability that extends beyond the founder. Track record matters too — not just revenue growth, but evidence that the management team has navigated difficult trading conditions, integrated acquisitions, or built new capability from a standing start. These are the signals that a business can continue to perform under new ownership.

Market position: the moat assessment

The final layer of investor analysis focuses on the structural position of the business within its market. Generalist freight forwarders operating across all modes, trade lanes, and verticals without particular depth in any of them face the most difficult valuation conversations. Specialism commands a premium — whether that is vertical expertise in a high-complexity sector such as pharmaceuticals, aerospace, or project cargo, or dominant positioning on specific trade corridors where relationships with carriers and agents are genuinely hard to replicate.

Geographic footprint is assessed both for its revenue contribution and for its strategic value to a potential acquirer. A regional forwarder with exceptional depth in Southeast Asian trade lanes may be worth considerably more to a global integrator than its standalone earnings would suggest. Brand reputation and the quality of long-standing shipper relationships round out this assessment — in an industry where trust is built slowly and lost quickly, reputation is a tangible asset.

Summary

Enterprise value in freight forwarding is not a mystery, but it is frequently misunderstood. The businesses that achieve the highest multiples are not necessarily the largest or the most profitable in absolute terms. They are the ones that have built earnings which are sticky, scalable, and defensible — revenue that does not walk out the door when a senior salesperson leaves, operations that do not require proportional headcount growth to expand, and technology that compounds in value rather than depreciates through dependency.

For operators building toward an exit — or simply building toward a better business — the framework is consistent. Revenue quality matters more than revenue size. Operational architecture matters more than operational reputation. Technology ownership matters more than technology adoption. And management depth matters more than management talent at the top.

The multiple a freight forwarder commands in the market is, ultimately, a verdict on the confidence an investor has that the earnings of today will persist and grow under their stewardship. Building that confidence is not a pre-sale exercise. It is the work of running the business well, from the inside out, over a long period of time.

Freight forwarding has always been a people-driven business. Relationships, operational know-how, and the ability to “get things done” have traditionally defined success.

But the operating environment has changed. Manpower is tighter, expectations are higher, and the volume of data that needs to be processed has increased significantly.

Today, many forwarders are not struggling because they lack business. They are struggling because they cannot scale operations efficiently with the manpower available.

a) The Manpower Challenge in Freight Forwarding

The industry is facing a structural manpower issue that is unlikely to reverse anytime soon.

1. Limited appeal to younger talent

Freight forwarding is not seen as an attractive career by younger professionals. Compared to tech or finance:

Work is operationally intensive

Career paths are unclear

Much of the work is still manual and repetitive

As a result, companies struggle to attract and retain new entrants.

2. Foreign manpower constraints

In markets like Singapore:

Governments impose quotas on foreign workers

Levies increase the cost of hiring

Work pass restrictions limit flexibility

This creates a situation where even if demand exists, companies cannot easily scale headcount.

3. Rising cost of manpower

With limited supply:

Salaries increase

Experienced staff become harder to replace

Attrition becomes more damaging

The result is a structurally tight labour market where growth is constrained by headcount.

b) Data Entry Dependency and Operational Fragility

While freight forwarding is perceived as a logistics business, much of its daily work is actually data processing.

1. Data entry-heavy areas in freight forwarding

Key processes rely heavily on manual data input:

Quotation creation Entering rates, surcharges, transit times, and routing options

Booking and job creation Capturing shipment details from emails, PDFs, or customer instructions

Documentation House bills, master bills, manifests, customs declarations

Billing and invoicing Matching charges, applying tariffs, ensuring accuracy

Milestone updates Tracking shipment status across multiple systems

In many cases, the same data is entered multiple times across systems.

2. What happens when staff are on leave or sick

Operations in many forwarders are still highly dependent on individuals.

When key staff are unavailable:

Jobs are delayed because others are unfamiliar with the files

Errors increase due to lack of context

Customers experience slower response times

Billing gets pushed out, affecting cash flow

Work doesn’t stop. It piles up.

3. Over-reliance on “super users”

Most organizations have a handful of experienced staff who:

Know the systems inside out

Understand exceptions and edge cases

Can fix issues quickly

These “super users” become bottlenecks:

Everything escalates to them

They carry institutional knowledge in their heads

When they leave, capability drops immediately

This creates operational risk that is rarely documented.

4. Scalability limitations

If growth requires proportional increases in headcount, the model is not scalable.

Common symptoms:

More volume = more hiring

More hiring = more training

More training = inconsistent quality

At some point, the organization hits a ceiling where:

Hiring cannot keep up

Quality starts to decline

Margins are squeezed

c) How AI Can Help Address These Challenges

AI is not about replacing people. It is about reducing dependency on repetitive tasks and improving consistency.

1. Automating data capture

AI can extract structured data from:

Emails

PDFs

Excel sheets

Customer instructions

Instead of manually typing:

Shipment details are captured automatically

Data is validated against expected formats

Missing fields are flagged immediately

This reduces the time spent on job creation significantly.

2. Reducing reliance on individuals

AI systems can:

Learn standard workflows

Apply predefined business rules

Handle routine decision-making

This means:

Less dependency on specific individuals

More consistent output across teams

Faster onboarding of new staff

3. Supporting exception management

Rather than processing every shipment manually, AI allows teams to focus on exceptions:

Flag unusual routing or pricing

Detect missing charges

Highlight inconsistencies between documents

Operations shift from:

“Process everything manually” to “Review only what looks wrong”

4. Improving scalability

With AI support:

Volume can increase without proportional headcount growth

Existing teams can handle more shipments

Service levels remain stable even during peak periods

This changes the operating model from manpower-driven to capability-driven.

5. Enhancing data quality

AI can continuously check:

Field accuracy

Data consistency across systems

Historical patterns

Better data leads to:

More reliable reporting

Faster billing cycles

Improved decision-making

Summary

Freight forwarding is facing a structural shift.

Manpower is constrained, costs are rising, and the traditional model of scaling through headcount is no longer sustainable. At the same time, operations remain heavily dependent on manual data entry and a small number of experienced individuals.

This creates a fragile system where growth, service quality, and profitability are constantly under pressure.

AI offers a practical way forward. By automating data capture, reducing reliance on individuals, and enabling teams to focus on exceptions rather than routine processing, forwarders can operate more efficiently with the resources they already have.

The goal is not to remove the human element from freight forwarding. It is to allow people to focus on what actually adds value while technology handles the repetitive work in the background.

Those who make this shift will not just reduce costs. They will build operations that are scalable, resilient, and better positioned for the future.

Freight forwarding is often misunderstood from the outside. On paper, it looks like a high-revenue business moving large volumes of cargo across the globe. In reality, it operates on tight margins, complex processes, and constant pressure on cost and pricing.

Many forwarders focus heavily on growing revenue. Fewer take a hard look at what actually remains at the bottom line. The uncomfortable truth is this: in a low-margin industry, small inefficiencies can quietly erode a large portion of profit.

To understand where the opportunity lies, we need to look at three things:

What the industry actually earns

Where profit is lost

How technology, particularly AI, can help recover it

A) Average Net Margins in Freight Forwarding

Across the industry, net margins are consistently low.

Large global players such as Kuehne+Nagel, DSV and DHL Global Forwarding typically operate within a 3% to 6% net margin range under normal market conditions.

Mid-sized and regional forwarders generally fall between 2% and 5%, while smaller forwarders often operate at 0% to 3%, with many hovering around break-even.

Margins can temporarily expand during strong market cycles, as seen during the pandemic, but structurally the business remains tight.

This leads to a simple but critical conclusion:

Freight forwarding is not a margin expansion game. It is a margin protection game.

B) Revenue Leakage: Where Profit Disappears

Revenue leakage is rarely the result of one major failure. It is the accumulation of small, everyday issues across the shipment lifecycle.

1. Operational Data Inaccuracies

Incorrect weights or volumes

Wrong chargeable calculations

Misaligned shipment details (POL, POD, Incoterms)

These errors often result in underbilling or missed billing entirely.

2. Incomplete Cost Capture

Missing surcharges (PSS, GRI, congestion fees)

Accessorial charges not recorded

Vendor invoices not matched properly

In many systems, especially when automation is enabled, small discrepancies can pass through unnoticed.

3. Delayed or Incorrect Billing

Jobs closed late

Revenue posted in the wrong period

Manual corrections leading to credit notes

This affects not only revenue accuracy but also financial reporting and forecasting.

4. Sales–Operations–Finance Misalignment

Quotes not fully aligned with execution

Costs incurred outside of quoted scope

Poor handover between teams

This creates gaps where services are delivered but not fully monetized.

5. Process Gaps and Manual Workflows

Reliance on spreadsheets or email instructions

Lack of validation checks

High dependency on individual experience

These environments are prone to inconsistency, especially when workload increases.

The Financial Impact

Industry experience and internal assessments across forwarders consistently point to 1% to 3% of revenue lost through leakage.

That may sound small. It is not.

If a company operates at a 3% net margin:

A 2% revenue leakage effectively reduces profit by up to two-thirds

In some cases, it can eliminate profit entirely.

Most forwarders are not losing money because of pricing. They are losing money because they are not capturing what they already earned.

C) How AI Can Reduce Revenue Leakage

This is where AI starts to shift the conversation. Not as a replacement for people, but as a control layer that continuously monitors and validates operations.

1. Data Validation in Real Time

AI can check shipment data against historical patterns and business rules:

Flag unusual weight-to-volume ratios

Detect incorrect routing or missing fields

Identify inconsistencies between booking, execution, and billing

Instead of relying on periodic audits, issues are identified as they occur.

2. Automated Charge Verification

AI can compare:

Quoted charges vs. executed services

Vendor invoices vs. expected costs

Applied surcharges vs. applicable conditions

This ensures that all billable items are captured before invoicing.

3. Exception-Based Management

Rather than reviewing every shipment, AI highlights:

Missing charges

Margin deviations

Late job closures

Teams focus only on exceptions, improving both efficiency and accuracy.

4. Pattern Recognition and Learning

Over time, AI learns:

Typical customer behaviors

Common operational errors

Seasonal or trade lane variations

This allows the system to proactively flag risks before they become financial issues.

5. Continuous Monitoring Without Fatigue

Unlike manual processes:

AI does not overlook small values

AI does not slow down during peak periods

AI does not depend on staffing levels

It provides a consistent control mechanism across the business.

Summary

Freight forwarding operates on thin margins, typically between 2% and 6%, depending on scale and market conditions. In such an environment, even small inefficiencies can have a disproportionate impact on profitability.

Revenue leakage, often in the range of 1% to 3% of revenue, is one of the most overlooked challenges in the industry. It stems from everyday operational gaps, data inaccuracies, and misalignment between teams.

The real opportunity is not just to grow revenue, but to protect it.

AI offers a practical way forward by introducing real-time validation, automated checks, and exception-based management. It allows forwarders to move away from reactive auditing and toward proactive control.

In a business where margins are tight and competition is high, the companies that succeed will not necessarily be the ones that sell more.

They will be the ones that capture what they already earn.

On one side, digital-native players have shown that technology alone does not guarantee success. On the other, traditional forwarders that resist modernization risk gradual erosion of competitiveness.

The real challenge is not choosing between “digital” or “traditional.” It is aligning business economics with the right technology — in the right sequence.

Many forwarders fail not because they lack software, but because their strategy, processes, and systems are misaligned. This is where structured business alignment becomes critical.

The Core Problem: Strategy and IT Often Move Separately

In many organizations:

The management team defines commercial targets.

Operations focus on service execution.

IT implements tools in isolation.

The result is fragmented transformation.

Systems are installed without redesigning processes. Automation is introduced without cleaning master data. AI tools are layered onto inconsistent workflows.

Technology becomes an expense instead of a performance lever.

True digitization begins with business alignment — not software selection.

What Business Alignment Really Means

Business alignment in freight forwarding involves answering fundamental questions:

Which customer segments are truly profitable?

Which trade lanes generate consistent margin?

Where does operational cost leak?

Which processes create bottlenecks?

How exposed is the company to rate cycles and working capital strain?

Without clarity on these fundamentals, digitization becomes cosmetic.

Alignment means defining:

A clear commercial strategy

A disciplined pricing and procurement model

Standardized operational workflows

Measurable performance indicators

A realistic digital roadmap

Only then should technology be layered in.

The Role of Modern IT Partners

Forwarders do not need to build technology internally. They need to integrate the right capabilities.

Modern IT providers in the logistics sector offer solutions such as:

AI-driven data extraction from emails and documents

Automated rate management systems

Digital booking interfaces

Carrier integration tools

Compliance automation

Visibility and control tower platforms

But tools must serve a defined objective.

For example:

If quoting speed is the issue, implement structured rate databases and automated comparison engines.

If margin leakage is the issue, implement profitability dashboards and financial controls.

If operational errors are frequent, automate document validation and milestone tracking.

The mistake is adopting tools without linking them to measurable business outcomes.

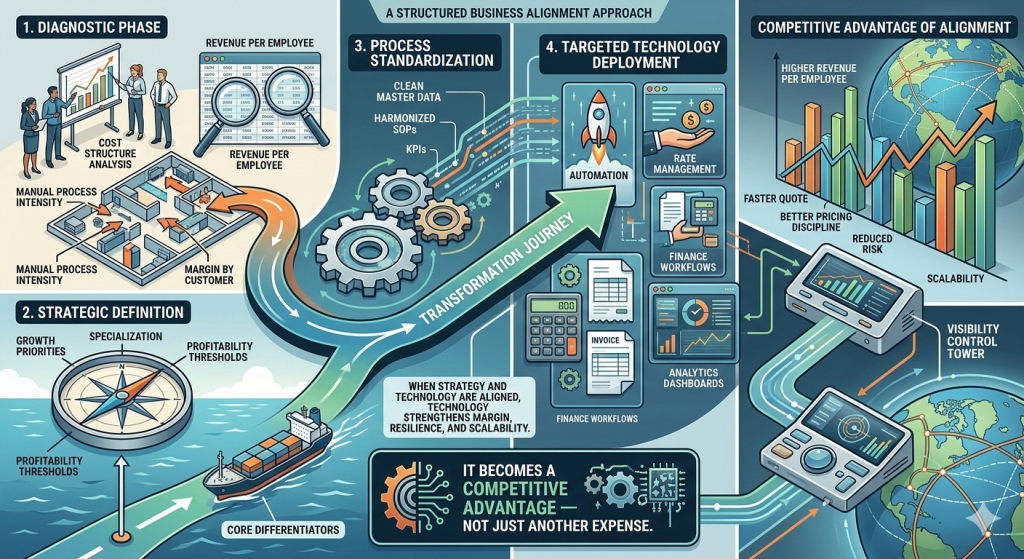

A Structured Transformation Approach

Effective transformation follows a clear sequence:

1. Diagnostic Phase

Analyze cost structure

Review revenue per employee

Identify manual process intensity

Map margin by customer and trade

2. Strategic Definition

Define growth priorities

Clarify specialization areas

Set profitability thresholds

Identify core differentiators

3. Process Standardization

Clean master data

Harmonize SOPs

Define escalation logic

Create measurable KPIs

4. Targeted Technology Deployment

Introduce automation in repetitive tasks

Implement rate management tools

Integrate finance workflows

Deploy analytics dashboards

This ensures that technology enhances economics rather than obscuring weaknesses.

The Competitive Advantage of Alignment

When strategy and technology are aligned, forwarders gain:

Higher revenue per employee

Faster quote turnaround

Better pricing discipline

Reduced operational risk

Stronger capital control

Scalability without proportional headcount growth

Digitization becomes a profit amplifier — not a branding exercise.

Why External Guidance Matters

Internal teams often struggle with transformation because:

Operational teams are absorbed in daily execution

IT teams focus on implementation, not strategy

Leadership lacks neutral benchmarking

An external advisory partner can bridge commercial strategy and technical execution, ensuring that:

Business objectives drive system selection

IT investments are prioritized based on economic impact

Implementation avoids unnecessary complexity

Change management is structured and realistic

This prevents both under-digitization and over-investment.

Summary

Freight forwarding is not saved by technology alone, nor protected by tradition alone.

The companies that will lead the next decade are those that:

Understand freight economics deeply

Define clear commercial priorities

Standardize and discipline operations

Deploy targeted, well-integrated technology

Digital transformation is not about replacing people with software.

It is about aligning strategy, process, and systems so that technology strengthens margin, resilience, and scalability.

When business alignment comes first, IT becomes a competitive advantage — not just another expense line.

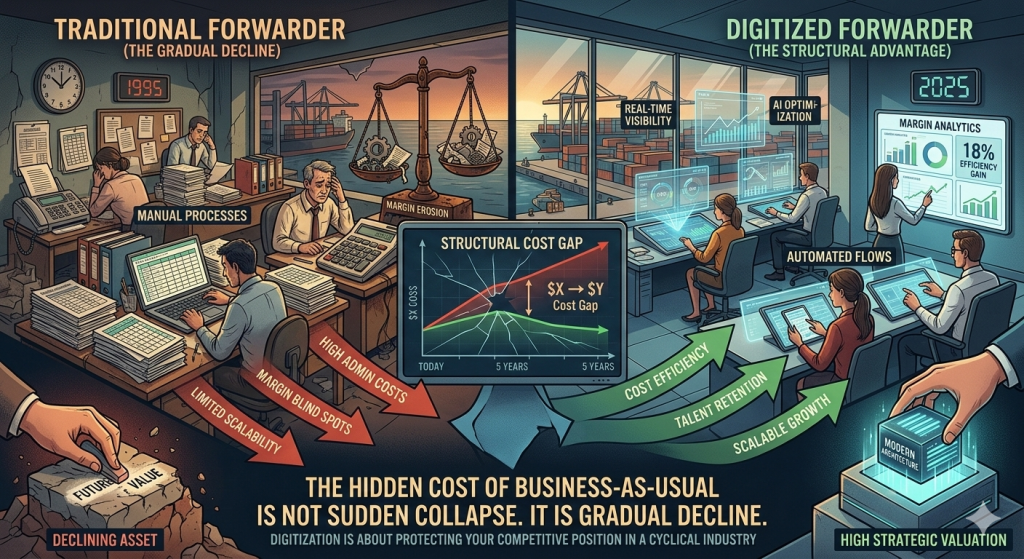

For many traditional freight forwarders, the business case for digitization can feel overstated. If margins are stable, customers are loyal, and operations run “well enough,” the urgency to modernize may appear low.

After all, freight forwarding has survived decades of change.

But the real risk of failing to digitize is not sudden collapse. It is gradual competitive erosion. Forwarders that continue operating under a business-as-usual model may remain profitable in the short term — yet steadily lose structural advantage in the long term.

The danger is not disruption. It is decline.

1. Structural Cost Disadvantage

Digitized competitors operate with:

Fewer people per shipment

Lower error rates

Automated billing cycles

Faster quote turnaround

Better margin visibility

Over time, this creates higher revenue per employee and stronger cost efficiency.

Traditional forwarders that rely on manual processes carry higher administrative costs. Initially, this may not be visible. But as automation spreads, cost gaps widen.

Eventually, competitors can either:

Undercut pricing while maintaining margin, or

Reinvest efficiency gains into sales and growth

The non-digitized forwarder becomes structurally less competitive.

2. Margin Blind Spots

Manual systems often mean:

Fragmented rate data

Limited real-time profitability tracking

Inconsistent branch-level reporting

Delayed financial visibility

Without integrated data, pricing discipline weakens. It becomes harder to:

Identify unprofitable customers

Track margin erosion by trade lane

React quickly to carrier rate changes

Digitization does not guarantee higher margins — but it enables transparency. Without that visibility, forwarders risk making decisions based on incomplete information.

3. Increasing Customer Expectations

Large shippers increasingly expect:

API connectivity

Automated document exchange

Real-time milestone visibility

Data reporting dashboards

Integration with ERP systems

Even if customers tolerate manual processes today, procurement standards evolve.

Forwarders unable to meet digital interface requirements may find themselves excluded from tenders — not because of poor service, but because of integration limitations.

Gradually, they are pushed toward smaller accounts and more price-sensitive segments.

4. Talent Drain and Operational Fragility

Non-digitized operations often rely heavily on individual experience and informal knowledge.

This creates two risks:

Key-person dependency — when senior staff leave, operational stability weakens.

Over time, the organization becomes less scalable and more vulnerable to turnover.

Digitization distributes knowledge across systems rather than individuals.

5. Limited Scalability

Manual operations can handle moderate volume efficiently — but scaling requires proportional headcount increases.

Digitized forwarders can grow shipment volume faster without linear staff growth.

Traditional forwarders face a choice:

Hire more people to grow

Or cap growth to maintain control

Both limit long-term expansion potential.

6. M&A and Valuation Pressure

In consolidation cycles, buyers increasingly value:

Standardized systems

Clean data architecture

Integrated reporting

Automated workflows

Forwarders that fail to digitize may still be profitable — but their valuation multiples may suffer due to modernization costs required post-acquisition.

In other words, they remain viable businesses but become less attractive strategic assets.

7. Risk Exposure in a More Complex World

Trade compliance, sanctions regimes, ESG reporting, and customs regulation are becoming more complex.

Digitized systems allow:

Automated compliance checks

Data-driven audit trails

Faster regulatory reporting

Manual models increase exposure to errors, fines, and compliance breaches.

In a world of tightening regulation, process control becomes a competitive advantage.

Summary

Freight forwarders that fail to digitize will not disappear overnight. Strong relationships and disciplined economics can sustain them for years.

But the risks accumulate gradually:

Higher structural costs

Reduced margin visibility

Exclusion from digital tenders

Talent attrition

Scalability limits

Lower strategic valuation

Digitization is not about following a trend. It is about protecting competitive position in an industry where margins are thin and cycles are unforgiving.

In freight, survival depends on economics. In the long run, economics depend on efficiency.

And efficiency increasingly depends on digital capability.

Over the past decade, a new generation of “digital freight forwarders” promised to reinvent logistics. With modern interfaces, automated booking flows, real-time dashboards, and AI-driven rate comparisons, they positioned themselves as technology companies operating in freight.

The assumption was clear: digitize the process, remove inefficiencies, scale rapidly — and profitability would follow.

Yet several high-profile digital players have faced layoffs, valuation cuts, strategic pivots, or closures. The problem was not a lack of technology. The problem was forgetting the economics of freight.

The Illusion: If It’s Digital, It Must Be Better

Companies such as Flexport, Forto (formerly Freighthub), Xeneta, and Haven built models centered around:

Automation

Platform visibility

Data-driven rate comparisons

Reduced manual intervention

Technologically, these models were impressive. Operationally, they improved transparency and efficiency.

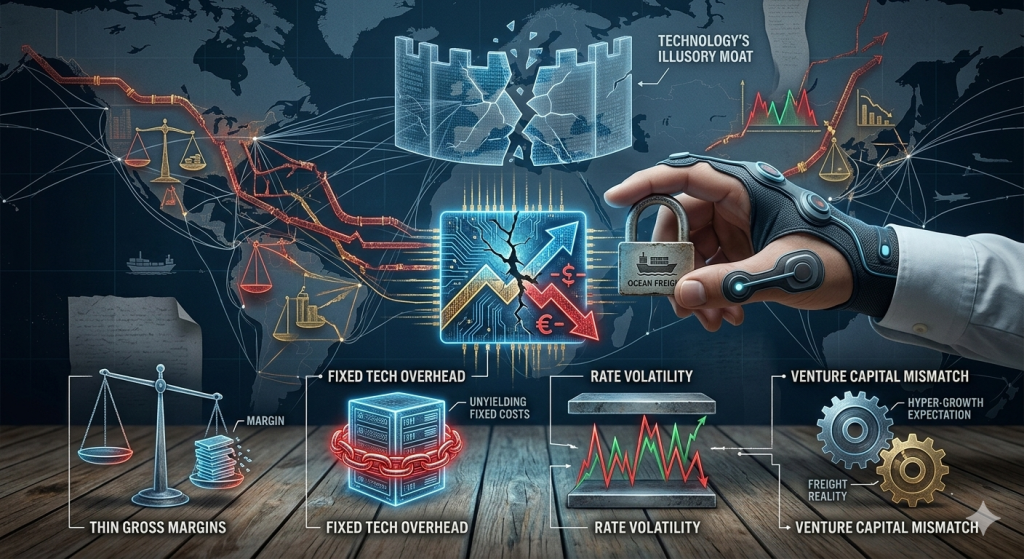

But freight forwarding is not a software business. It is a cyclical, capital-intensive, low-margin industry.

Digitization improves execution. It does not rewrite industry structure.

Freight Has Structural Realities

Freight forwarding operates under constraints that technology alone cannot eliminate:

Thin gross margins

High working capital requirements

Exposure to volatile carrier rates

Customer price sensitivity

Credit risk

Relationship-driven procurement

When ocean and air rates surged during the pandemic, digital forwarders scaled aggressively. Revenue rose rapidly. Valuations expanded.

When rates normalized, the underlying economics reappeared.

This mismatch creates tension. To meet growth targets, digital forwarders often prioritize volume expansion over margin discipline. In freight, volume without pricing power can destroy profitability.

Traditional forwarders, by contrast, often grow slower but guard margins more carefully.

Technology Adds Cost Before It Adds Advantage

Another misconception is that digital means lean.

In reality, digital forwarders carry:

Large engineering teams

Product and UX staff

Data infrastructure expenses

Marketing and brand spend

These are fixed costs.

When margins compress, high fixed costs become dangerous. Traditional forwarders can reduce operational staff quickly in downturns. Tech-heavy models have less flexibility.

Digitization reduces manual labor, but if the tech overhead is too high relative to freight margins, the cost structure becomes unstable.

Freight Is Not Purely Transactional

Freight is full of exceptions:

Port congestion

Sanctions and compliance issues

Space allocation politics

Disputes over demurrage and detention

Credit and liability negotiations

Shippers still value escalation handling, commercial judgment, and relationships with carriers and authorities.

Digital interfaces may simplify booking, but when complexity arises — and it always does — the real value lies in operational depth and risk management.

If technology replaces too much of the relationship layer without strengthening the control layer, the model becomes fragile.

What Was Overestimated

Digital forwarders often assumed:

Shippers would switch primarily for better UI

Carriers would fully expose rates digitally

Automation would dramatically increase margins

Freight could scale like software

In practice:

Switching costs in freight are operationally high

Carrier relationships remain strategic

Margin gains from automation are incremental, not transformative

Freight cycles compress profitability regardless of platform quality

Technology is necessary infrastructure. It is not a structural moat.

The Core Problem: Ignoring Economics

The central issue is not digitization failure. It is economic misalignment.

Freight profitability depends on:

Pricing discipline

Procurement leverage

Customer mix

Working capital control

Risk management

Cost flexibility

If these fundamentals are weak, digitization simply accelerates volume through an unprofitable engine.

You can build the most elegant booking interface in the industry. If you misprice risk or overextend working capital, the model breaks.

The Real Lesson

Digital freight forwarders are not failing because they are digital.

They struggle when they assume digitization replaces freight fundamentals.

The sustainable model likely lies in combining:

Strong economic discipline

Lean but effective digitization

Careful cost control

Operational depth

Capital resilience

Technology should strengthen margins, not mask them.

Freight remains what it has always been: A cyclical, risk-sensitive, relationship-heavy industry.

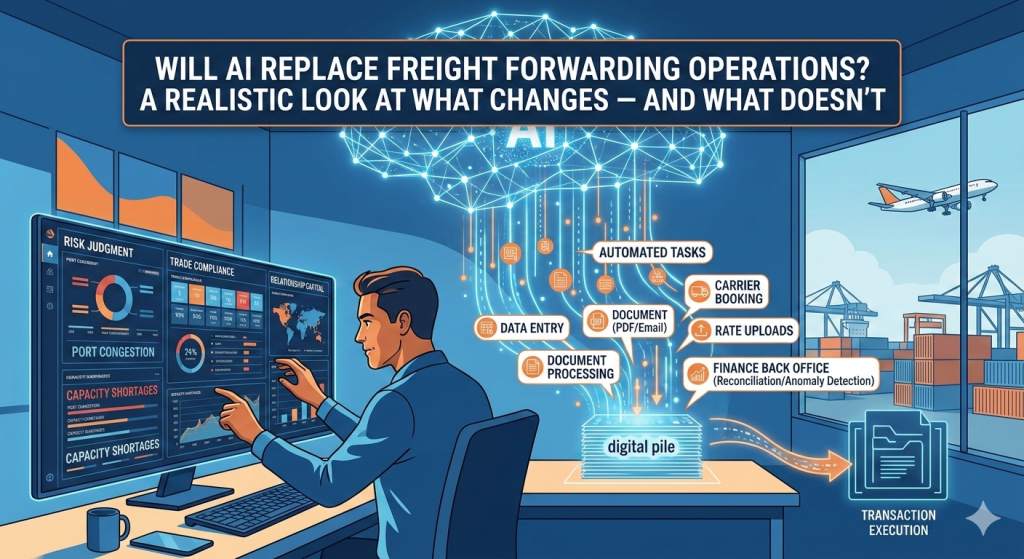

There is a growing belief that freight forwarding is on the brink of a major workforce reduction. The logic seems straightforward: if artificial intelligence can handle bookings, customs interfaces, documentation, invoicing, and reporting, then the need for large operational teams should disappear.

At first glance, this argument is compelling. Much of freight forwarding is process-driven, repetitive, and rule-based. These are precisely the areas where AI performs well.

But while AI will significantly reshape operations, it will not eliminate the structural complexity of freight. The future will not be “no humans.” It will be fewer transactional roles and more judgment-driven roles.

Understanding that distinction is critical.

What AI Will Replace

AI will dramatically reduce manual work in three core areas:

A. Data Entry and Document Processing

Shipment creation, milestone updates, draft BL checks, invoice matching, rate uploads, customs documentation formatting — these tasks are structured and repetitive.

AI systems already extract, validate, and populate structured data from emails, PDFs, and messaging platforms. Over time, these functions will require minimal human intervention.

B. Transaction Execution

Carrier booking, routing selection, rate comparison, and service validation can all be automated when rate data is structured and business rules are defined.

Technically, AI is capable of executing bookings and validating service conditions. The real barrier is not capability — it is data cleanliness and system integration.

C. Finance Back Office

Accounts receivable reminders, payables matching, statement reconciliation, margin reporting, and even intercompany netting are highly rules-based.

AI-driven anomaly detection can flag discrepancies, while automated workflows manage routine processes. Finance teams will shrink in size but become more analytical in focus.

In short, repetitive operational roles will decline significantly.

What AI Will Not Easily Replace

Despite these gains, freight forwarding is not purely transactional. Several areas resist full automation.

A. Risk Judgment Under Uncertainty

Freight operates in constant ambiguity:

Port congestion Sanctions and trade compliance risk Capacity shortages Sudden regulatory changes Customer credit exposure

AI can detect patterns, but strategic trade-offs under uncertainty require experience. Deciding whether to prioritize a volatile high-margin customer over a stable long-term client is not just data-driven — it is commercial judgment.

B. Relationship Capital

Freight is still relationship-heavy, especially in tight markets. Securing space during peak season, negotiating demurrage waivers, extending credit terms, or resolving customs bottlenecks often depend on human trust and networks. AI does not build that capital.

C. Accountability and Liability

When shipments fail, delays occur, or claims arise, companies need accountable individuals.

Contracts are signed by humans. Negotiations are handled by humans. Liability cannot be delegated to an algorithm.

The Likely Future Structure

The forwarder of the future will not eliminate people. It will reorganize them.

A plausible structure includes:

Commercial Core: Strategic sales, pricing specialists, key account managers Control Tower / Exception Team: Escalation managers, compliance experts, risk controllers Technology & Data Layer: AI oversight, system integration, data governance Procurement & Carrier Relations: Contract negotiation and capacity strategy Lean Finance: Oversight and financial analytics

The large middle layer of shipment processing executives will shrink. Revenue per employee will rise. The organization becomes more concentrated around high-value decision-making.

The Hidden Constraint: Data Quality

All of this depends on clean master data, structured rate databases, standardized SOPs, and integrated systems. AI does not fix disorganized processes. It amplifies them. Companies that digitize chaotic foundations will not see transformative results. Companies that clean their data and standardize processes first will benefit the most.

Where Differentiation Moves

As AI absorbs transactional work, competitive advantage shifts.

It will no longer be about:

Faster booking input Cheaper documentation processing Invoice accuracy Instead, differentiation will center on: Industry specialization Risk management capability Network strength Financial stability Advisory capability for customers

AI will significantly reduce repetitive operational roles in freight forwarding. Data entry, transaction execution, and back-office processing will become increasingly automated.

However, freight remains a cyclical, risk-sensitive, relationship-driven industry. Strategic judgment, accountability, and trust cannot be automated away.

The future is not a human-free forwarder. It is a leaner organization where low-value tasks disappear and high-accountability roles increase in importance.

In practical terms, AI will compress the middle layer of operations — but elevate the value of leadership, commercial strategy, and risk management.